← Notebook

← Notebook

Three times this month, I have been sent the same article wearing a different hat.

SaaS is dead. AI agents will replace the software stack. Citizen developers will rebuild the vendor landscape over a long weekend. We can cancel the renewals, delete the procurement calendar and use the savings for something cheerful.

It is an appealing story. It is also the latest in a long line of technology funerals where the deceased keeps turning up to work.

I have spent twenty-five years in enterprise architecture across oil and gas, banking, media, government and insurance. In that time, I have attended several solemn farewells for technologies that are still sending invoices. Client-server was going to kill the mainframe. Cloud was going to kill the data centre. Low-code was going to kill the developer.

Each prediction was directionally right and operationally wrong. The technology changed. The old thing lost some territory. Then the awkward machinery of real organisations turned up and refused to fit inside the headline.

So rather than asking whether SaaS is dead, I think there are three more useful questions:

- What actually dies?

- What survives?

- Who gets handed the bill?

Answer those and the funeral becomes something much more useful: a renewal strategy.

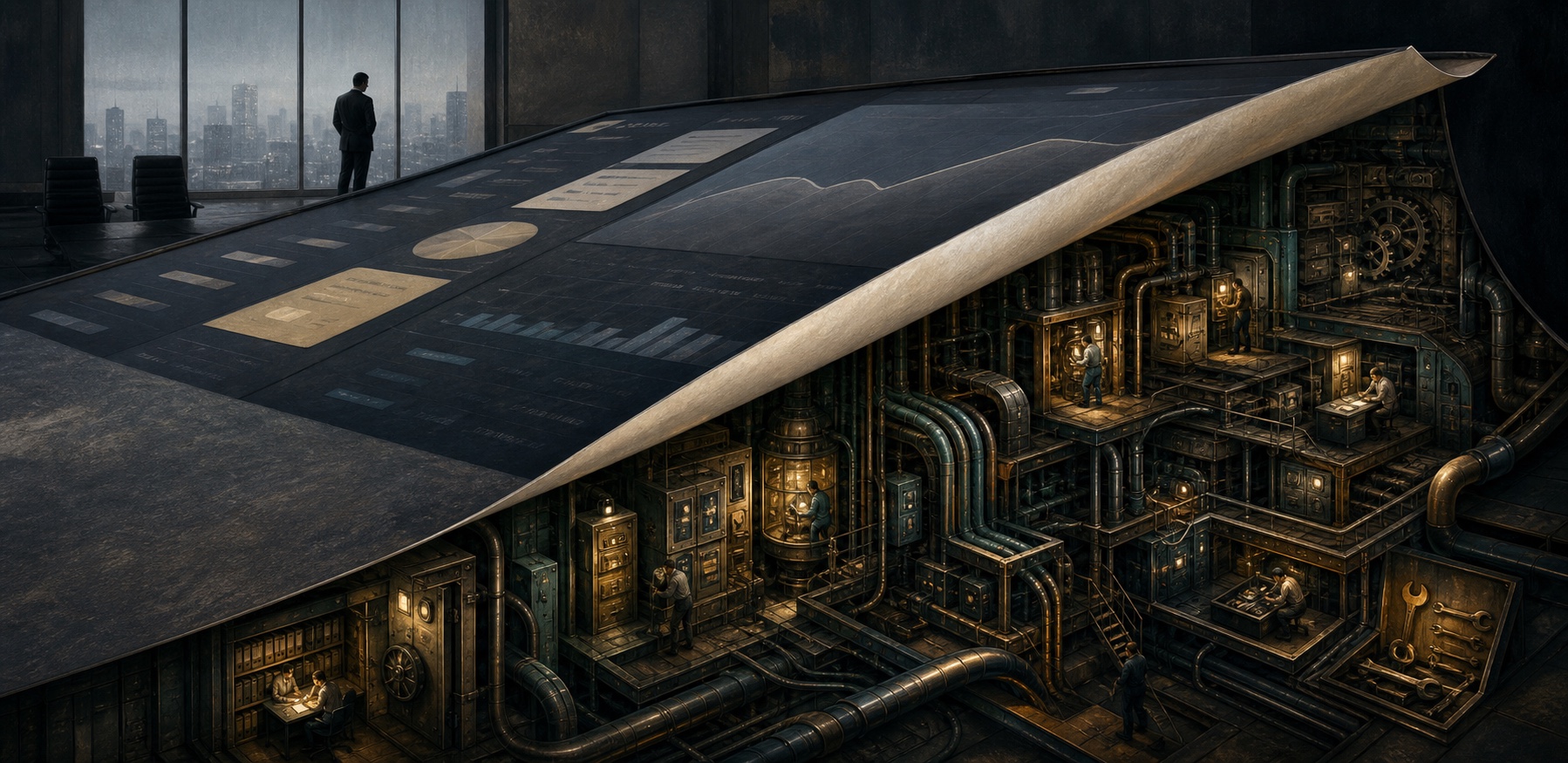

The interface is becoming free. The obligation is not.

Building was never the moat

The standard argument begins reasonably enough. AI has made it much easier to build the “organise and display” layer of software. Point an orchestrator at the right data and ask for an approvals pipeline, a case-management screen or a small reporting tool, and the result can be surprisingly good.

If a machine can build the thing in an afternoon, why are we paying a vendor per person, per month, forever?

The trouble is hiding in the verb. AI is making it cheaper to build that layer. It has not made it free to operate it.

Operating software means access reviews, audit trails, privacy controls, data retention, support, monitoring, integration changes and recovery when something quietly stops working on a public holiday. It means knowing what a model update changed, why an automated decision was made, and who is responsible when the answer is “apparently nobody”.

It also means coping when the person who assembled the whole thing leaves with the only reliable map of how it works. This tends to happen shortly before something important changes upstream. Computers enjoy timing.

A ten-person business can absolutely replace a small point solution with something AI helped build on Tuesday. A ten-thousand-person organisation may be able to do the same technically, but that is not the whole purchase. The vendor was also providing a roadmap, a support organisation, a compliance posture and somebody contractually obliged to answer the telephone at two in the morning.

A weekend app is not a system of record.

That does not make the weekend app bad. It makes it a different species.

What dies: software whose only moat was inconvenience

Some SaaS products are genuinely exposed. The selection pressure is not “can AI rebuild the interface?” It usually can. The better question is: once the interface and routine workflow are cheap, what remains that the customer cannot easily reconstruct?

A point solution built from a clean database, a dashboard and a firm opinion about how work should flow now has a thin moat. For years, the inconvenience of rebuilding it was part of the product’s protection. AI has handed customers a reasonably capable ladder.

This does not mean every thin-moat product disappears next Thursday. Procurement cycles, integrations, habits and fear of breaking payroll are all excellent preservatives. But at renewal time, “our screens are nicer” becomes a much weaker argument when new screens can be produced before the steering committee has agreed on the colour palette.

The most exposed products are likely to share a few traits:

- their data is already owned by the customer;

- their workflow is common rather than specialist;

- their integrations are shallow or replaceable;

- switching does not threaten a regulated or revenue-critical process; and

- their price depends on customers believing that rebuilding is much harder than it now is.

Strip away the interface and ask what is left. If the answer is mostly a schema and some confidence, start planning.

What survives: the things AI cannot regenerate

Now consider an accounting platform. Its interface can be copied. Its basic workflow can be copied. Many of its reports can be copied.

What cannot be summoned from a prompt are years of bank-feed agreements, tax integrations, accumulated edge cases, audit acceptance and customer trust. Those things are not code. They are relationships and obligations that have survived contact with reality.

The same applies elsewhere. A healthcare platform may have clinical integrations and regulatory standing. A logistics platform may have a network of carriers and years of exception data. A marketplace may have buyers, sellers and the delicate machinery that keeps them from fleeing at the same time.

AI can rebuild the screens. It cannot rebuild the relationships.

This is where the “SaaS is dead” argument becomes too blunt to be useful. SaaS is not one species. Some products rent a convenient workflow. Others provide access to an ecosystem, a trusted record or a set of connections that would take years to reproduce.

The first group is under pressure. The second may become more valuable, provided it does not confuse owning the moat with being entitled to neglect the customer.

The seat is wobbling, not disappearing

The next popular prediction is the death of per-seat pricing. If one AI agent can do work previously spread across fifty people, the customer is unlikely to keep paying for fifty identical seats out of nostalgia.

That part is difficult to argue with. The seat is a poor measure of value when software is doing more of the work itself.

The tidy replacement is “outcome pricing”: charge per resolved ticket, processed invoice, completed review or successful result. It sounds modern, aligned and pleasingly simple.

Then somebody asks what next year will cost.

Enterprises do not buy only capability. They also buy budgetability — not the most elegant word in the language, but a very popular one in finance. Pure usage pricing turns a predictable line item into a variable cost whose most expensive month may also be the month when the business is already having a difficult time.

What is more likely is a hybrid: a platform fee for access, support and predictable capacity, plus a consumption element for agentic work. It is messier than the keynote version and much harder to explain with one ascending arrow.

Which is usually a sign that it may survive contact with an actual budget.

Who eats the margin?

This is the part of the shift I find most revealing, and it receives much less attention than the funeral notices.

Traditional SaaS could often serve one more user at very little additional cost. AI-driven software is different. When the product reads documents, reasons across them, generates an answer or runs an agentic workflow, somebody pays for the compute each time it happens.

That does not make AI software uneconomic. It does mean the cost structure changes, and the industry must decide where that recurring cost lands.

There are three obvious candidates.

The vendor can absorb it, accepting lower margins in exchange for keeping prices attractive. The customer can absorb it through higher or usage-based prices, where the value of the work is clear enough to justify the bill. Or the infrastructure providers can reduce it over time as models, hardware and competition make inference cheaper.

In practice, all three will happen in different parts of the market. Vendors will redesign products to use expensive models only where they matter. Customers will demand caps, tiers and the return of that reassuring old friend, the predictable invoice. Infrastructure providers will compete to make intelligence feel less like a metered luxury.

The strategic clues will be in pricing changes, product bundling, model choices and vertical integration — not in how many times the word “agentic” appears in the launch announcement.

Follow the margin, not the headline.

The awkward bit: timing

None of this gives us a reliable timetable.

Structural pressure can take years to become structural change. Incumbency is a powerful anaesthetic. A large CRM platform does not survive only because its workflow is defensible. It survives because migrating twenty years of customer history, integrations, permissions, reports and unofficial workarounds is a programme nobody is eager to fund.

Data gravity is inertia wearing a strategy costume.

That inertia gives incumbents time. Some will use it to deepen the things customers cannot recreate. Others will add a chat panel, rename three menu items and wait for the applause. The market will not treat those strategies equally forever, but “forever” is doing important work in that sentence.

There is another limitation. AI will not progress evenly. Some workflows are forgiving; others carry legal, financial or human consequences that make verification and accountability central. The easier it is to check and reverse the work, the faster a home-grown alternative can spread. The harder it is to explain or undo a mistake, the more valuable a credible operator remains.

Direction is not timing. A sensible portfolio strategy needs both, and should not pretend to have the second merely because the first makes a good slide.

Three questions for your next renewal

If you own an application portfolio — or simply a collection of software subscriptions that has begun breeding when nobody is looking — take these questions into the next renewal.

- What is the moat once the interface is cheap?Look for data, integrations, accreditation, network effects and trusted relationships. “We know your workflow” is useful, but it is no longer enough on its own.

- Who carries the operational obligation if we rebuild it?Price the five-year burden honestly: support, controls, model changes, audit evidence, integration failures and the inevitable departure of someone important. Do not compare a vendor’s full cost with only the first afternoon of your alternative.

- How exposed is the vendor to the new cost structure?Ask how AI usage is priced, what happens at scale and whether the roadmap depends on economics that no longer apply. A vendor can be optimistic. Your exit plan should not have to be.

Products that fail all three tests should not be ripped out in a burst of enthusiasm. They should be exited deliberately, on your timetable, before somebody else’s business model chooses the date for you.

The mutation, in one sentence

SaaS is not dying. It is being forced to reveal what customers were really paying for.

Where the answer is merely a static interface and an inconvenient workflow, AI will push the price down and alternatives will multiply. Where the answer is trusted data, embedded relationships, operational accountability and access to a functioning ecosystem, the vendor still has a job — and possibly a very good one.

The era of renting every static tool by the seat is beginning to fray. What replaces it will not be a vendor-free paradise assembled over a long weekend. It will be a more demanding market in which software companies have to earn rent from the parts of the service that cannot be regenerated before lunch.

What dies? Convenience pretending to be a moat.

What survives? The difficult obligations and relationships underneath the software.

Who gets handed the bill? Watch closely. That answer will tell us what the next software industry actually looks like.

And then comes the governance question: what happens when the tools your organisation depends on are the ones nobody formally owns?